Making the Most of Down Payment Assistance Programs MABA MassachusettsRealEstate FirstTimeHomeBuyers MaBuyerAgent

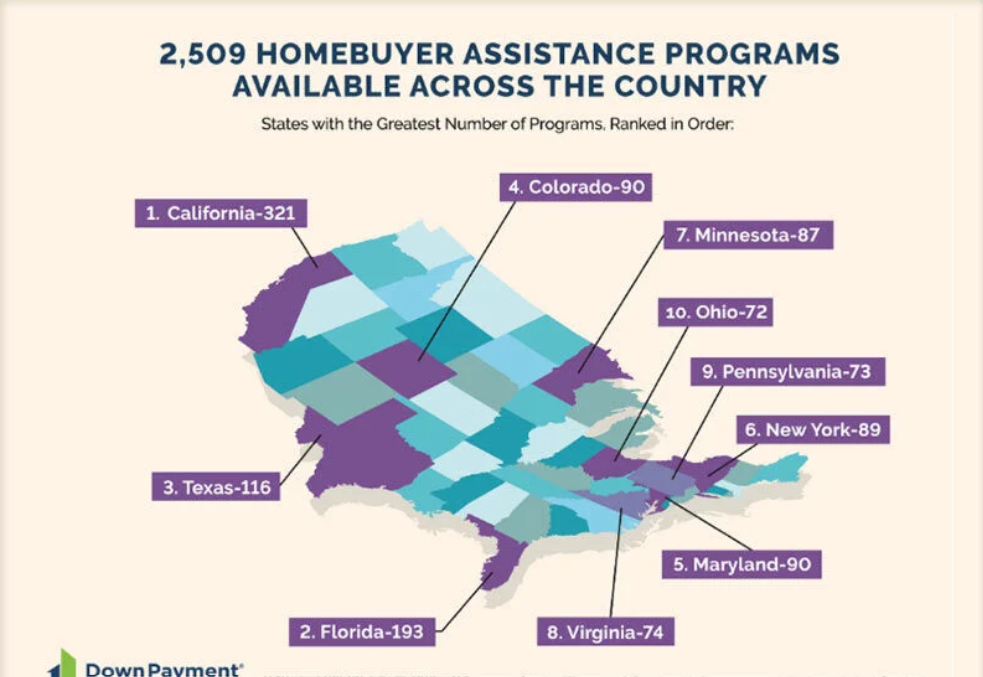

The latest Q1 2025 Homeownership Program Index (HPI) report from Down Payment Resource (DPR) found the number of entities offering homebuyer assistance programs increase by fifty five year-over-year (YoY). The number of programs increased by forty three during the first quarter, bringing the total number of available programs to two thousand five hundred and nine.

Downpayment assistance (DPA) can be used by lenders to lower a homebuyer’s loan-to-value (LTV) ratio by an average of six percent. The average benefit is eighteen thousand dollars.

“Rates are still high and prices keep climbing, but we’re seeing expanded program offerings, new providers and greater flexibility in how funds are used—not just for downpayments, but also to cover closing costs, lower the rate or meet other buyer needs,” said Rob Chrane, Founder and CEO of DPR. “More programs now include manufactured and multifamily homes, opening new paths to affordability and steady income. For lenders, that means more ways to qualify buyers and close loans in a tough market.”

The latest Freddie Mac Primary Mortgage Market Survey (PMMS) found the thirty year fixed-rate mortgage (FRM) at six point eighty three percent as of April 17, 2025, up from the previous week when it averaged six point sixty two percent. A year ago at this time, the thirty year FRM averaged seven point one percent.

The post Making the Most of Down Payment Assistance Programs first appeared on The MortgagePoint.

FIRST TIME HOMEBUYERS

"The MABA agent helped us find the perfect home for us at the right price and we felt extremely good about the final deal."

Article From: "Eric C. Peck" Read full article

Get Started with MABA

For no extra cost, let a MABA buyer agent protect your interests

800-935-6222 Call now!

How to Make Better Homebuying Decisions

Who Pays a Buyer’s Agent?

![]()