Mortgage Payments Jump Again in October MABA MassachusettsRealEstate FirstTimeHomeBuyers MaBuyerAgent

With the national median payment requested by purchase applicants rising to $2,127 from $2,041 in September, homebuyer affordability decreased in October. This is in line with the Mortgage Bankers Association‘s (MBA) Purchase Applications Payment Index (PAPI), which uses information from the MBA Weekly Applications Survey (WAS) to calculate how new monthly mortgage payments change over time in relation to income.

“Homebuyer affordability conditions declined notably in October as rapidly rising mortgage rates pushed the national median mortgage payment up eighty six dollars from September,” said Edward Seiler, MBA’s Associate VP of Housing Economics and Executive Director for Research Institute for Housing America. “With the increase in mortgage rates, the PAPI reached its highest level since July, and we expect weaker homebuyer affordability to remain a hurdle for prospective buyers in the final months of 2024.”

The mortgage payment to income ratio (PIR) is larger when the MBA’s PAPI rises, which is a sign of deteriorating borrower affordability conditions. This can be caused by rising mortgage rates, growing application loan amounts, or a decline in earnings. When loan application amounts, mortgage rates, or incomes decline, the PAPI declines, which is a sign of improving borrower affordability conditions.

Key Findings of MBA’s PAPI: October 2024

- The national median mortgage payment was two thousand one hundred and twenty seven dollars in October—up eighty six dollars from September. It is down by seventy two dollars from one year ago, equal to a three point three percent decrease.

- The national median mortgage payment for FHA loan applicants was one thousand eight hundred and forty two dollars in October, up from one thousand seven hundred and fifty three dollars in September and down from one thousand nine hundred and fifty five dollars in October 2023.

- The national median mortgage payment for conventional loan applicants was two thousand one hundred and thirty four dollars, up from two thousand and fifty three dollars in September and down from two thousand two hundred and eight dollars in October 2023.

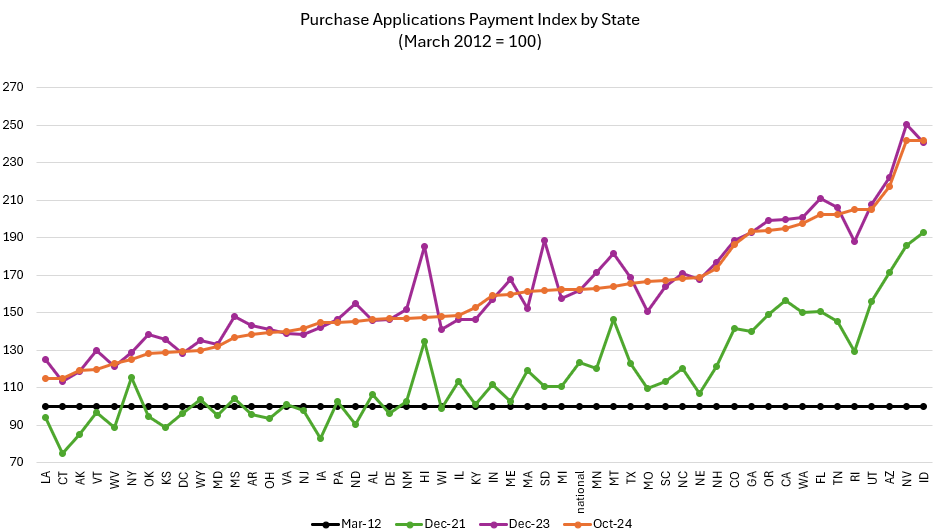

- The top five states with the highest PAPI were: Idaho (two hundred and forty one point nine), Nevada (two hundred and forty one point six), Arizona (two hundred and seventeen point two), Utah (two hundred and five point one), and Rhode Island (two hundred and five).

- The top five states with the lowest PAPI were: Louisiana (one hundred and fourteen point eight), Connecticut (one hundred and fifteen point one), Alaska (one hundred and nineteen point one), Vermont (one hundred and nineteen point six), and West Virginia (one hundred and twenty three).

- Homebuyer affordability decreased for Black households, with the national PAPI increasing from one hundred and fifty seven point nine in September to one hundred and sixty two point three in October.

- Homebuyer affordability decreased for Hispanic households, with the national PAPI increasing from one hundred and fifty point one in September to one hundred fifty four point two in October.

- Homebuyer affordability decreased for White households, with the national PAPI increasing from one hundred and sixty point two in September to one hundred and sixty four point seven in October.

The national PAPI rose from one hundred and fifty seven point nine percent in September to one hundred and sixty two point three percent in October, a two point eight percent rise. While payments fell three point three percent, median wages increased three point two percent, and the PAPI is down six point three percent annually as a result of the modest earnings rise. The national mortgage payment rose from $1,369 in September to $1,431 in October for borrowers who applied for lower-payment mortgages (the 25th percentile).

MBA’s national mortgage payment to rent ratio (MPRR) declined from oine point forty six at the end of the second quarter (June 2024) to one point thirty four at the end of the second quarter (September 2024), implying mortgage payments for house purchases have reduced compared to rents.

In Q2 of 2024, the HVS national median asking rent, as reported by the Census Bureau, rose to $1,523 ($1,481 in the same quarter). In September, the ratio of the median asking rent to the 25th percentile mortgage application payment dropped to 0.90 from 0.99 in June 2024.

The median mortgage payment for purchase mortgages from MBA’s Builder Application Survey rose from $2,333 in September to $2,470 in October, according to the Builders’ Purchase Application Payment Index (BPAPI).

To read the full report, including more data, charts, and methodology, click here.

The post Mortgage Payments Jump Again in October first appeared on The MortgagePoint.

FIRST TIME HOMEBUYERS

Buyer’s Agents Explained

HOMEBUYERS BEWARE! Book Review

This book is an excellent first step in a complicated process.

BEWARE the cards are stacked against you! Get Tom Wemett's book, learn why are different from other

Buying a home is like buying a car, on steroids. It’s the biggest investment you are likely to make so the stakes are incredibly high. I knew that having an agent represent me was a good idea.

What I hadn’t grasped was how important it is to find one who is not connected with the selling side in any way—through an agency that also represents sellers, as most do, at least in Mass. In researching buyer agents, I found Tom through the Mass. Assoc. of Buyer Agents (MABA).

Article From: "Demetria C. Lester" Read full article

Get Started with MABA

For no extra cost, let a MABA buyer agent protect your interests

800-935-6222 Call now!

How to Make Better Homebuying Decisions

Who Pays a Buyer’s Agent?

![]()